#2 - Real World DeFi - The Elephant in the Room

#2 - Real World DeFi - The Elephant in the Room

Welcome to this second episode of Real World DeFi - The Elephant In the Room

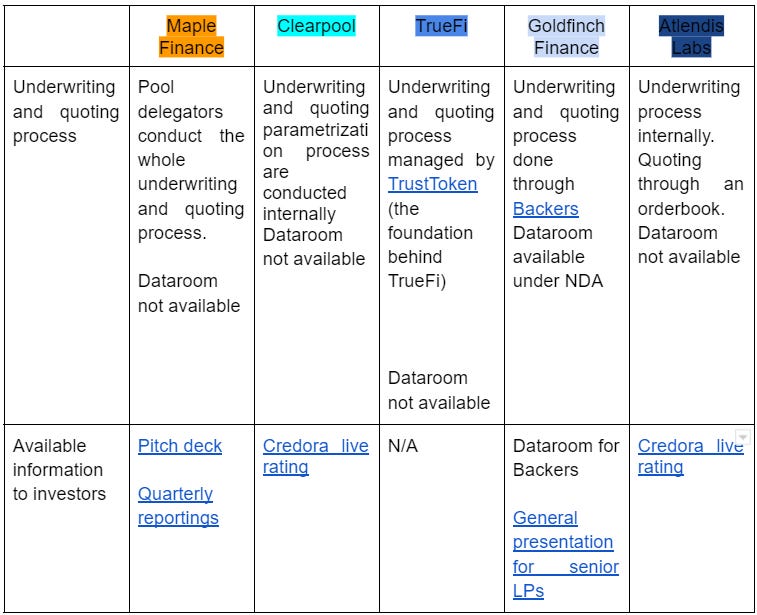

Underwriting, scoring, quoting : the Trinity of credit protocols

Decentralized credit protocols have uneven processes when it comes to underwriting loans on their platforms.

Underwriting, which leads to risk scoring (the probability that the counterparty will default and not repay) but also interest and repayment terms should not be overlooked.

Today, most of this information is not accessible to the common investor and the underwriting and scoring is often carried out internally.

Sources: Maple : Pitch deck , Quarterly reportings, Clearpool: Credora live rating, Goldfinch: General presentation for senior LPs, Atlendis Labs: Credora live rating

Only two platforms allow to have a look on the financial health of a borrower in real time with Credora. There is a need for a generalisation of the use of scoring (for 3) as well as a greater transparency on the rating given (for all).

Most protocols give access to very general information on loans.

It would be appropriate to have an idea of the sector of activity, the geographical area and the default history per borrower.

Transparency on the real-world legal documents signed between the counterparties and the protocol.

Access to a dataroom under NDA for key members such as Goldfinch is also a great initiative.

Assurance of alignment of interest is one of the fundamental principles of trust in the protocols, and to show who has it, transparency is the foundation.

We will detail this part specifically in another episode.

Maker’s DAI Endgame Plan : to RWA or not to RWA ?

A little bit of context :

The DAI is a stablecoin pegged to the dollar that historically operates with an over-collateralisation mechanism. People deposit 1.5USD worth of ETH to mint 1 DAI.

It's a proven mechanism, with no major depeg since 2019 despite high market volatility.

But this overcollateralization mechanism has one big flaw, its capital inefficiency.

It is hard to scale DAI market cap as it needs to collateralize an even bigger value of asset as collateral.

Indeed, DAI market cap reached $10B and shrinked to $7Bn in current conditions. DAI accounts for approx. 1% of total crypto-assets market capitalisation and ranks as the fourth most popular stablecoins far behind USDC ($50Bn), USDT ($68Bn) and BUSD ($21Bn).

DAI market cap as not grew as it peers due to this limiting capital efficiency characteristic.

That's why Maker has been more and more attracted to financing DAI through the real economy and real world asset financing as part of its aggresive growth strategy.

The scheme is straightforward: DAI is issued in the form of loans to financial institutions investing real world projects in many industries : real estate, infrastructure to name a few. These institutions pay back interests and principal in the form of DAI to Maker according to the loan conditions.

The amount of DAI in circulation increases without having to put more collateral aside and after repayment some DAI still remains in circulation thanks to interest payments. Also, DAI is backed by the future interest proceeds from the issued loans.

DAI is now scalable, but risk mitigation is the key:

One/Maker governance has to be sure that the risk of default would not exceed the interest rate otherwise newly issued DAI would bear bad debt and peg would be weaken as DAI in circulation are not backed anymore by real proceeds. Thus, the need for maker to source a bunch of independent loans, with amount below surplus buffer (i.e. exposure) so as to minimise massive liquidation/bankruptcy scenario.

In a nutshell:

Better capital efficiency and therefore better scalability

More income for MakerDAO

Risk mitigation plans to implement : adequate loan risk scoring and underwriting

This medium article enters further details about how Maker is working : D3M, Peg stability, RWA

However, despite all these evolutions, some MakerDAO members are concerned about DAI development through RWA and are opposed to the current roadmap Maker is heading towards.

Voices like Rune's (Maker core founder) are being heard within Maker's governance to put at least a temporary halt to this integration.

Why ?

In the wake of the US regulators' sanctions against Tornado Cash, Rune points to what he calls the "post 9/11 paradigm", i.e. the US regulators' obsession with security despite freedom. This can be translated for the financial world as a schism between fully compliant activities and others that are automatically classified as dangerous for society.

With the fall of CeFi lenders and Terra, the opportunity to show regulators that basing one's infrastructure on blockchain technology has been missed.

The possibility of seeing its activity frozen overnight and without warning like Tornado Cash is a concrete possibility for him.

There are two options: either Maker becomes fully compliant and transforms itself into a neo-bank or it moves away from regulatory constraints by being as decentralised and virtual as possible.

The only way to do this, according to him, is to limit the exposure to the RWA of the DAI and thus to make the DAI free-floating.

Indeed, since the demand for DAI would have difficulty being sustained by supply due to the lack of $ETH backing, the only way to maintain demand for DAI would be through negative interest rates which would act to reduce the demand for DAI.

Maintaining a strong free-floating DAI would be achieved through a Protocol Owned Vault (to own liquidity) and Meta DAOS (to provide broader use cases for DAI) that are described as the Endgame plan in his governance post.

Not all Maker DAO members agree on this theory and development path, which leaves room for rich debates that this twitter thread deciphers very well.

This debate shows both the difficulty of having a vision and a clear project within a DAO (a reversal of the situation after Maker joined RWA two years ago), the fear of the regulator as an inhibitor of financial innovation and an on-chain world that could stand on its own.

The question that arises today is to know the balance of power that exists between the global regulators (especially American) and the spokespersons of the new financial paradigm created thanks to DeFi.

Finance has always coexisted with compliance to develop economies, it is necessary to ensure that the balance of power is healthy with the regulator and this means giving more and more utility to DeFi.

The carbon markets and its on-chainization

Carbon markets are regulatory tools that facilitate the achievement of all or part of politically determined greenhouse gas (GHG) emission reduction targets.

Carbon markets can take the form of regulated or voluntary markets.

Regulated markets have been implemented since the Kyoto Protocol in 1997, when it was stipulated that companies belonging to certain polluting industries had to limit their polluting capacity to certain pre-established quotas. Exceeding these allowances by a company can only happen if it buys allowances from another company that has not used them all.

These regulated markets have been developing at a slow pace for the past twenty years due to the conflicting interests of countries and companies in engaging in this system.

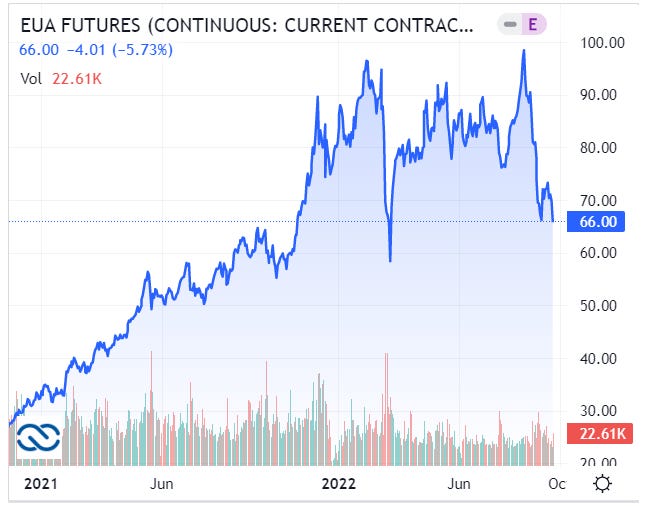

The EU Emissions Trading System is now the most successful market on a supra-national scale with a volume of $683bn or 90% of the global trading volume ($760bn) and market value ($270bn).

The other side of the carbon markets are voluntary markets. These markets, deployed at multiple scales, allow emitters to offset their irreducible emissions by purchasing carbon credits from projects labeled as reducing or removing GHGs from the atmosphere.

In recent years and with the push for corporate ESG policies, these markets have been growing rapidly but are still much smaller than the regulated $2 bn markets in 2021.

What is a carbon credit and what are its characteristics ?

The instruments that are traded on the carbon markets are carbon credits.

A “carbon credit” is a permit that gives the holder the right to emit, over a certain period, carbon dioxide or other greenhouse gasses (e.g. methane, nitrous oxide or hydrofluorocarbons). 1 carbon credit corresponds to 1 metric tonne of carbon dioxide prevented from entering the atmosphere.

On regulated markets these credits take the form of Assigned Amount Units (AAUs) which correspond to an allowance to emit one metric tonne of CO2 or equivalent greenhouse gas due to the fact that another company has given up using this credit.

In the voluntary markets, a company will buy a carbon credit to offset one metric tonne of CO2 already emitted. The carbon credit here represents "1 tonne of CO2 removed or reduced" by a sustainable project.

Carbon credits are therefore issued in the framework of voluntary markets by sustainable projects that are financed through these instruments. These sustainable projects can take the form of :

Forestry and conservation: they account for the majority of projects. It enables carbon removing from the atmosphere to stock it into trees

Renewable energy : solar or wind farms are built to produce decarbonized energy.

Waste to energy : involving methane capture and conversion into electricity.

Sometimes the credits take on a more social dimension (e.g. : Water, Sanitation and Hygiene (WASH)) but with still a focus on reducing carbon emissions by changing habits of people : local forest protection, reduce smoke pollution etc.

One of the key elements behind these carbon credits is to ensure their quality through several criteria:

Measurability: Quantification of emission reductions and removals refers to the methodologies according to which emissions are measured

Credible baselines assess the emissions that would have been emitted to and/or removed from the atmosphere had the project or program not been implemented.

Assurance of additionality means that the carbon emission reductions and removals associated with a carbon credit would not have occured without the incentives and resources provided by a project.

Preventing and accounting for leakage refers to ensuring that a project avoids and does not simply displace GHG emissions

Assurance of permanence involves ensuring that each carbon credit generated represents a long-term climate benefit, that could be defined as 100 years.

What are the pillars for ensuring the quality of credits today?

Raters: Calyx Global, BeZero Ratings and Sylvera – are new entrants in this market, and seek to bring more transparency on verified carbon claims and deliver scores of different projects against each other. This approach mimics that of financial credit ratings or ESG ratings (scoring carbon offsetting projects using rating systems like AAA, BB, etc.). But, methodological approaches of some of these ratings agencies remain opaque

Standards: for example Verra or Gold Standard – are key organizations in the ecosystem that define methodologies and principles for project developers to follow.

Safeguards: ensure that voluntary carbon projects do not cause social and environmental harm.

Transparent and benefit sharing: ensures that local populations benefit from VCM activities. Benefits can accrue to communities in the form of direct payments, improved infrastructure, community services, or other non monetary benefits.

Limits

The carbon credit market is criticised from two main angles

Potential perverse effect of carbon credits

Carbon offsetting could create perverse incentives: organizations may be tempted to use carbon offsets to meet all their emission reduction targets, rather than making the investments necessary to significantly reduce their own carbon footprint. In this way, they would continue to run high-emission activities and invest in high-emission equipment and facilities. Some observers advocate treating carbon offsets as a complement to climate action, rather than as a primary means of mitigation.

Carbon Offset Quality

Despite the efforts of carbon offset programmes, a number of independent studies have identified serious problems with carbon offsets. For instance, studies (Alexeew et al. 2010; Cames et al. 2016; Gillenwater and Seres 2011; Haya and Parekh 2011) show that up to 70% of their offsets may not represent valid emissions reductions, other studies highlight some of carbon offset projects that resulted in broader environmental damage. An official report ordered by the United Nations in 2012 mention all the shortcomings and areas of potential improvement

How to be sure that forestry plantation to capture carbon for the next century will not burn into flames in five years ?

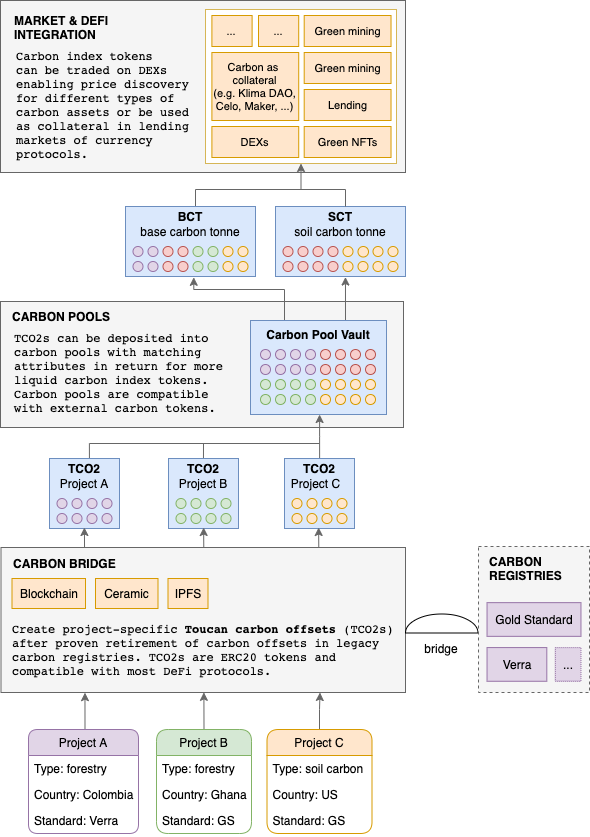

On-chain carbon

In the course of 2020 and 2021, several decentralized carbon credit projects have emerged, including Klimao Dao, Toucan Protocol, Moss Earth.

Both Toucan and Moss Earth implemented a bridging process in order to assign an on-chain tokenized representation to carbon credits.

As the voluntary carbon market suffer from opacity, plurality of assets without norms and lack of market accessibility, Toucan and Moss Earth both want to facilitate standardization and transparency to carbon credits.

Bridging processes

Thanks to these protocols, several concerns mentioned above could be addressed efficiently.

Once credit carbons are bought on-chain, the use of the proceeds could also be monitored if they are done through stablecoins. For instance, proceeds could be transferred to a list of whitelisted addresses corresponding to local communities or companies that are tied to the offsetting project.

Standards are difficult to impose. It might be much easier to do so with the help of protocols acting as aggregators.

To the same extent, knowing that a carbon credit has been effectively bridged after having been scrutinized over the given standard could facilitate the understanding of its quality : rating would mean more.

Carbon credit would still need raters, still need safeguard. However, imposing transparency would better align interest with the final buyers.

Besides, concerns on the perverse effect of offsetting through carbon credit as well as the lack of understanding on how carbon could be captured in the long term would not be solved :

Some metrics shows that the on-chain carbon market is still nascent and perfectible.

BCT and UBO tokens’ prices shrinked for the last two years whereas real carbon credit prices skyrocketed in the same period.

It tends to prove those assets 100% backed by carbon credit are not qualitative as the standard requirements or that the price was overestimated at first during the bullrun.

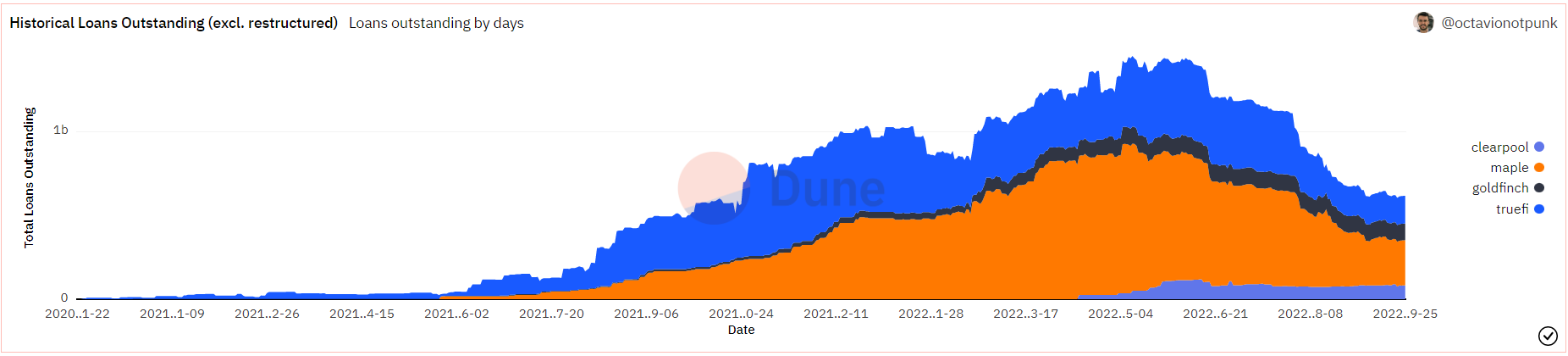

Protocols performance

A new dashboard is available for Polygon !

On Ethereum

New loans issued :

14 loans and ~$67M funded since September 12th

Outstanding Loans :

Maple : $291M ($269M on Dune but data is delayed, -$12M)

Goldfinch : $99M (~)

TrueFi : 165 (-$2M)

Clearpool : $81M (-$2M)

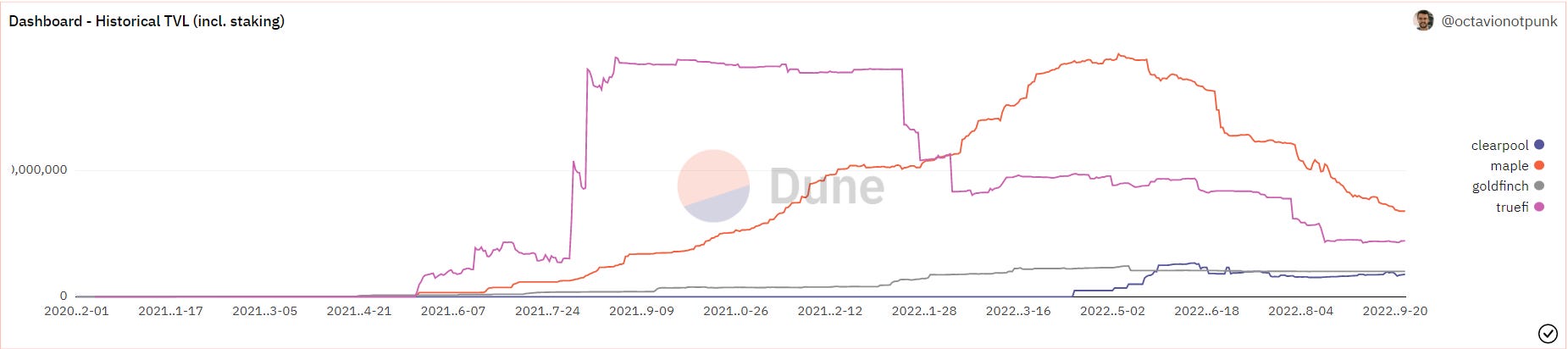

TVL (incl. staking) :

Maple : $340M ; (-$52M)

Goldfinch : $107M ; (~)

Truefi : $221M ; (+$2M)

Clearpool : $88M ; (-$2M)

APR (annual basis and excl. liquidity mining) :

Maple (projected) : 8.1%

Goldfinch (realized last 30 days): 10.8%

TrueFi (projected) : 9.3%

Clearpool (projected) : 4.8% (~7% on active pools)

Default :

0 in September

Active warning on Wintermute situation for Atlendis, Clearpool, Maple and TrueFi. Credora rating down from AA to A.