#4 - Liquidity premium, on-chain scoring and current market conditions

#4 - Liquidity premium, on-chain scoring and current market conditions

Elephant in the Room #4

Liquidity is the fountain of premium for thirsty investors

Spring is the fountain of love for thirsty winter ― Munia Khan

This episod reviews the notion of liquidity of financial assets, the associated premium and the fact that assets in decentralised finance do not escape it.

Definition and core principles

According to Investopedia:

“A liquidity premium is any form of additional compensation that is required to encourage investment in assets that cannot be easily and efficiently converted into cash at fair market value.”

The liquidity premium (or illiquidity premium, which refers to exactly the same concept) is a common observation that can be made in financial markets.

For example, a bond with a short maturity will tend to have a lower premium than a bond with a longer maturity. The liquidity premium is then one of the explanations behind the normal yield curve shape for bonds.

A bond with a relatively short maturity will tend to be more attractive than one with a long maturity, as the investor will be able to exit the investment more quickly.

A second manifestation of the notion of liquidity (and its premium) is the existence of secondary markets. A liquid asset could be exchanged on a secondary market for a value close or equal to the fair value, it is not the case for an illiquid at asset (as potential investors require a higher premium to make up for this risk).

Thus, assets with an existing and efficient secondary market generally offer lower rates of return than other assets with a similar risk profile but without access to these markets.

While the CAPM does not take into account this liquidity premium in its simplified model, studies such as Amihud and Mendelson (1986) show that in an imperfect world with market frictions, a liquidity premium naturally appears on financial assets.

Why do we talk about that:

Decentralised finance is an area of finance that has developed in a particular way.

Certain activities such as overcollateralized lending (with Aave, Compound), market-making within AMM (with Uniswap, Sushiswap) have brought to light exotic risks little known to market participants. Liquidation risk for borrowers, bad debt risk for lenders, or impermanent losses for liquidity providers on decentralized exchanges.

However, liquidity risk remained was not the most mentioned aspect of investment.

The reason?

Protocol designed in an extremely flexible way answering to the economic liberal rhetoric of crypto. ‘I want to have the right to dispose of my money at any time’ and ‘I want to avoid trusted third-party which are inherent to illiquidity assets.

The need for composability of protocols that build on top of each other.

A good illustration of this second point is Lido, a liquid staking protocol on top of Ethereum. stETH is a representation of ethereum staked on nodes indirectly operated by Lido (and its staking providers). This stETH can be used as a collateral on lending protocols such as Aave, to borrow other assets:

If a protocol uses tokens from another protocol that derives on other tokens, it must be ensured that the path to the underlying asset is as simple and low-risk as possible, hence extreme liquidity.

Expansion of DeFi to other use cases and appearance of liquidity premium

After the DeFi summer of 2020 focused solely on endogenous innovations (DeFi for DeFi), the ecosystem has gradually opened up to other innovations focused on a rapprochement with traditional finance concepts.

Whether it is with:

Undercollateralized credit protocols

Real-estate

Infrastructure, energy financing

or even 100% on-chain focused but with TradFi footprint:

Insurance with Nexus Mutual, InsurAce, Sherlock etc

Fixed yield product: Idle DAO, Notional, Sense, APWine etc.

Indeed, each of these categories must meet requirements that make it more difficult to resell the asset at its fair value.

Liquidity premium for undercollateralized loans

For on-chain undercollateralized loans it is not possible to exit at any time as the money can be lent off-chain.

For instance, Clearpool uses a curve pooling system to deter lenders to go out when there is scarce capital, and to oblige borrowers to reimburse otherwise they are in default.

If utilisation rate’s too low (i.e. a lot of capital provided for a low amount of borrow) interest is really low. It incentivises lenders to get out of the pool or the borrower to borrow more money as interest are low.

In the opposite situation, when utilisation rate too high borrowers should repay quickly loans because interests are costly and lenders really wish to increase their participation to the pool as the rate as juicy.

This curve shape reflect the liquidity premium: more interest is earned when there is a high utilisation rate.

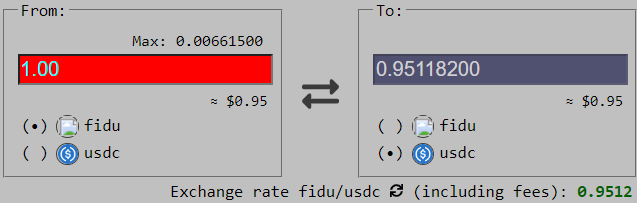

Besides, Goldfinch secondary market shows a discrepancy in the FIDU (pool token) price and its fair value:

FIDU Fair Value price : 1.09

FIDU secondary price on Curve : 0.95

FIDU secondary market price on Curve

Liquidity premium for on-chain insurance

As for Nexus Mutual, the liquidity premium is observed by the difference in price between the freely tradable wNXM token and the untradable NXM token representing pool shares.

In order to ensure effective coverage, Nexus Mutual must maintain a level of liquidity in its own funds equal to or greater than the minimum capital requirement.

The liquidity providers are unable to withdraw their money (and therefore to burn the NXM tokens) if the coverage ratio (coverage/liquidity) is too close to the MCR.

Acknowledging and mitigating predatory arbitrage

One of the particularities of DeFi is the presence of arbitrageurs who have the possibility to play with the difference between the fair price and the secondary market price instantly and seamlessly thanks to extreme DeFi composabilities.

For instance on Goldfinch, the primary market has been lacking liquidity for the past 6 months. It is not easy to redeem and withdraw directly from the pool because there is little to no cash available.

Moreover, as soon as a redemption takes place and cash is accrued within the pool, arbitrage bots will use it instantly (i.e. within a few blocks, or a few tens of seconds) to arbitrage the price difference with the secondary market. This results in the fact that ordinary investors can only rarely exit. (Nexus Mutual has the same problem between wNXM and NXM.)

Since there is a minimum capital requirement to insure the policies purchased, liquidity providers cannot exit when very rare occasions or premiums reported raise the available capital above the MCR and are arbitrated all the time by bots.

These are mechanisms that cannot be transposed to traditional financial markets and add an additional risk to liquidity.

However, this risk is manageable and removed by proper governance proposal:

- GIP-25 Goldfinch : create withdraw windows for liquidity providers. Investors can exit only to the ratio of the amount they are willing to release.

- Proposal Angle protocol : arbitrageur address whitelisting to align incentives between investors and arbitrageurs.

In a nutshell

The legacy of decentralised finance is illustrated by the extreme composability and liquidity of tokenised assets. As DeFi gets closer to the real economy, the lack of liquidity is necessarily something to be taken into account in the design of financial assets.

A golden rule to remember: two assets with the same characteristics will have two different yields depending on the liquidity inherent in each asset.

Scoooring

“The score will take care of itself when you take care of the effort that precedes the score.” ~ John Wooden

This article details Credora's scoring methodology and some of its limitations today.

Credora (formerly X-Margin), is the Infrastructure for Institutional Credit. It provides a credit worthiness ratings to financial entities with a score between 0 and 1000 (C to AAA).

Their ratings is only addressed to entities with a legal structure, activity report and an on-chain (through DeFi protocols) and off-chain (through centralized exchanges ) activity.

This score is composed of three parts

Operations and Due Diligence

The operation and due diligence pillar weight is 20% of the overall rating.

Due diligence:

Credora operates a due diligence process in which following risk factors are examined :

Compliance risk: including entity documentation and structure review,

Onboarding across reputable and regulated institutions,

Experience of key decision makers

Custodial infrastructure, including whether institutions use institutional grade solutions for CeFi and DeFi market access

Besides, Credora captures loans and repayment activity on platform and externally. The following factors are analyzed:

Length of borrowing history

Principal repayment history,

Active lending relationships,

Average collateralization on loans

Financial analysis

The financial analysis pillar weight is 40% of the overall rating.

This part is based on the statements of the rated companies (through financial reports), which must be updated at least quarterly.

The financials score considers:

Quality of Financial Statements: 1) Method of preparation 2) Recency of financials 3) Level of financial detail 4) Borrower accessibility

Performance: ROA/ROE, Maximum drawdown and solvency ratio

Debt Servicing: Solvency and liquidity ratio

Risk monitoring

The risk monitoring pillar weight is 40% of the overall rating.

This part is based on the data gathered from on-chain and off-chain real-times inputs off-chain (leading CeFi spot, derivatives, and custody venues) and on-chain (DeFi risk across Ethereum, Avalanche, BSC, Polygon, Fantom, 7 other EVM compatible networks)

Three factors are assessed thanks to these on-time data

Liquidity: visible assets on CeFi and DeFi versus assets reported on Financials. (20%)

Equity: visible equity on CeFi and DeFi versus assets reported on Financials. (10%)

Portfolio leverage: visible assets and liabilities on CeFi and DeFi versus those reported on Financials (10%)

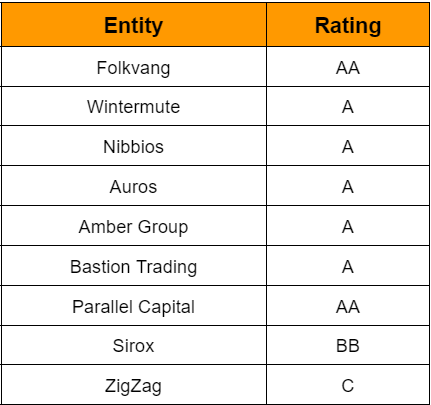

Entities scoring

Among the financial institutions that have a Credora public score and that have borrowed money in DeFi, we find that they have a fairly high score (above 800/equal to A).

The rating is not equivalent to the methods of traditional rating agencies.

Compound treasury (which offers a 4% fixed interest on its loans) was rated B- by S&P, equivalent to a junk bond, whereas it would have a rating of at least A according to the proxies with the entities rated by Credora.

Credora flaw and what it does not capture

Wintermute had two operational issues within a few months. Firstly the loss of control over a wallet containing optimism OP tokens (eq. $ 20m) then the hacking of several wallets with a loss of $160 million.

However, these two events did not lead to a downgrading of Wintermute's due diligence rating and only affected the risk monitoring rating. The score lowered from AA to A.

Counterintuitively, the rating of financial entities is quite opaque.

Publicly, only the final rating is available. To access more granular information (details by pillar and underlying data), one has to register on the platform and request the counterparty's permission. In a world where the controversial Moody's, Fitch and Standard & Poors publish their ratings of entities and states sometimes publicly, there is a dissonance with the ethos of open finance. Solutions exist, using zero knowledge proof to allow access to the final information without compromising the sensitive components of the calculations.

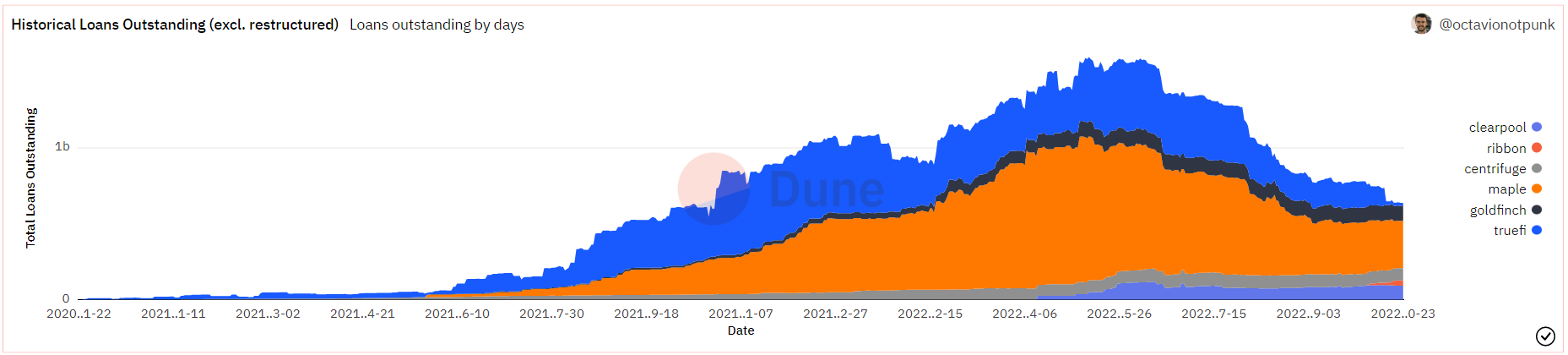

Protocols performance

Two protocols added: Ribbon and Centrifuge on Ethereum !

Polygon dashboard here

On Ethereum

New loans issued :

$6.5M on Maple

$2.5M on Centrifuge

~$15M on Ribbon

~$2M on Clearpool

Outstanding Loans :

Maple : $259M (-$23M) (To be changed in the dashboard)

Goldfinch : $99M (~)

TrueFi : 18 (-$104M) !!!

Clearpool : $90M (-$3M)

Centrifuge : $80M (+$1M)

Ribbon : $35M (+23M)

Default :

Full repayment of $92 million Wintermute loan on TrueFi

https://cointelegraph.com/news/wintermute-repays-92m-truefi-loan-on-time-despite-suffering-160m-hack